*** I will be in New York next week from 13-16 April. Please reach out if you would like to catch up ***

We have updated our comprehensive chartpack on labour markets in Australia and New Zealand.

Labour market outcomes in coming months will be key to central bank policy deliberations against a backdrop of rising and above-target inflation and the Middle East conflict.

For now, central banks will fret about inflation and inflation expectations, particularly those in economies with little spare capacity, including the RBA which we expect to tighten policy further in coming months.

Any signs of weakening labour market conditions, however, will provide central banks with some assurance that first-round inflationary effects of the conflict won’t leak into damaging second-round effects on inflation.

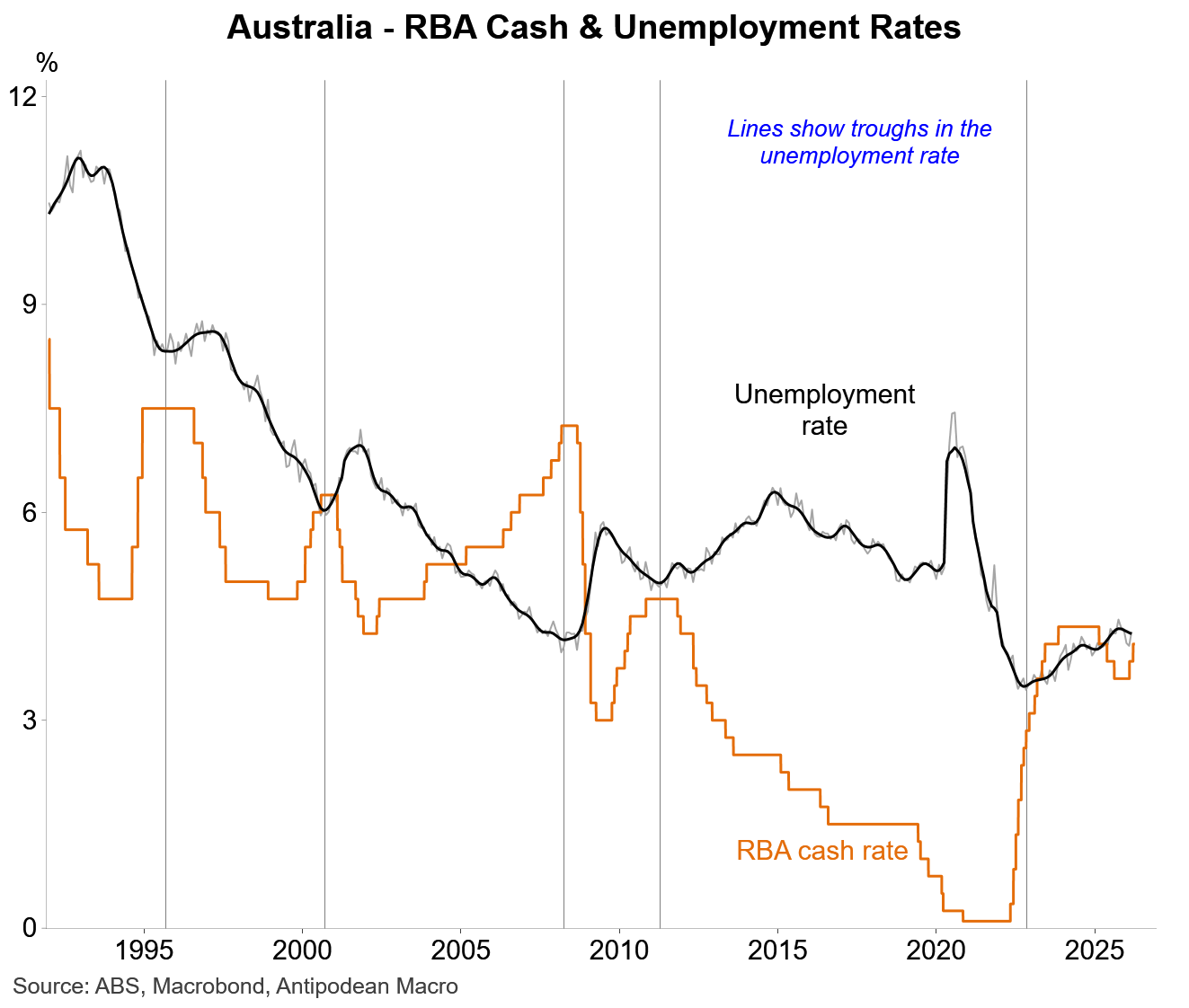

Historically, a rising unemployment rate has typically seen the RBA (and Fed) initially holding interest rates stable for a period of time before easing policy.

While rising inflation due to supply-side factors creates complexities for central banks, our view is that they will ultimately find it difficult to not act if unemployment rates persistently rise.

For the RBA, however, the jobless rate is clearly below that consistent with “full employment” and will need to rise to tame inflation.

For now, labour market conditions in Australia remain tight by historical standards and compared with most other advanced economies. While market-sector firms have lifted their hiring there is a risk that prolonged uncertainty will weigh on their appetite to take on more employees.