Australia’s Q1 CPI will be released on 24 April, a couple of weeks prior to the RBA Board meeting on 6-7 May.

Our bottom-up analysis points to relatively strong prints for both headline and underlying inflation.

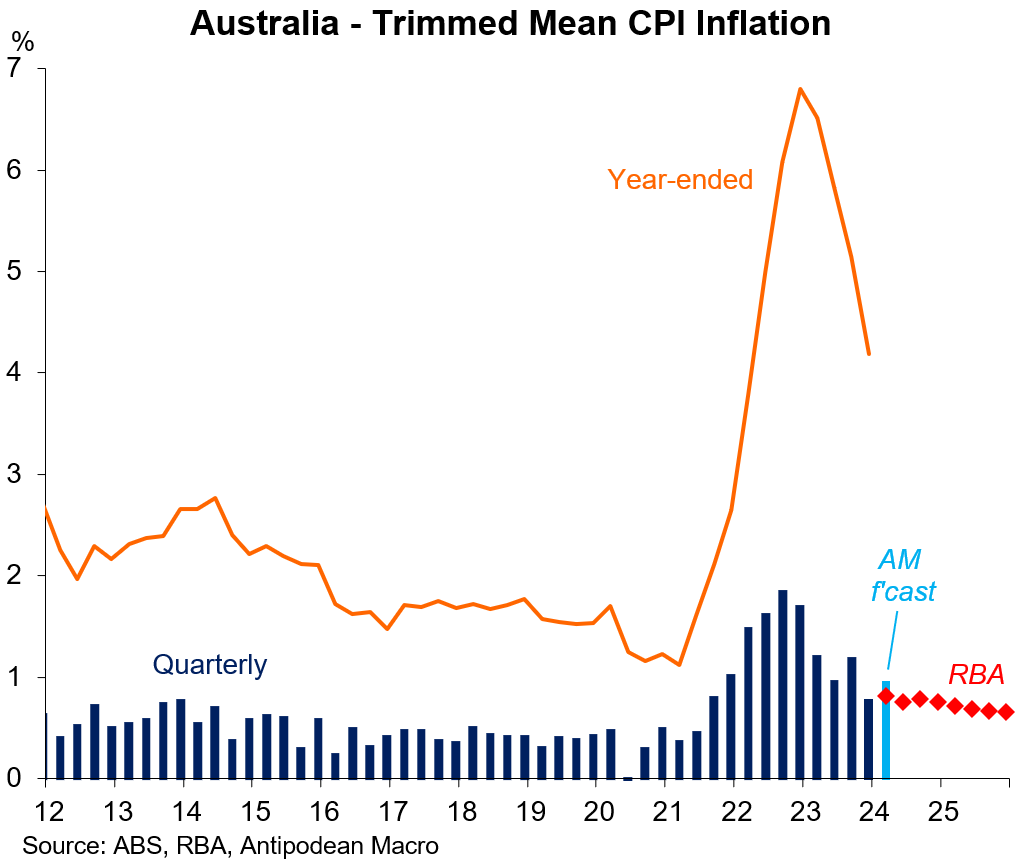

While Q4 inflation was softer than the RBA’s November SMP forecasts, we expect the Q1 print to be stronger than the RBA’s February SMP forecasts.

Part of the stubbornness of underlying inflation in Q1 is the normalisation of CPI rents inflation after it moderated in Q4 because of a large increase in government-provided rent subsidies. As we noted at the time, this had the effect of subtracting a bit less than 0.1ppts from both quarterly headline and trimmed mean inflation and needed to be kept in mind when thinking about the chances for further disinflation in Q1.

Key expectations

The monthly CPI for February - which printed in line with our expectations - provided key inputs to firm up ‘nowcasts’ of Q1 inflation. Our expectations are based on bottom-up estimates for all 87 CPI sub-components.

Headline CPI inflation is expected to have been 0.8-0.9% q/q and +3.5% y/y in Q1.

Our estimate for Q1 trimmed mean CPI inflation is 0.9-1.0% q/q and +3.9% on a year-ended basis. The RBA’s February SMP forecasts were +0.8% q/q and +3.8% y/y.

We don’t normally give ranges for our quarterly inflation forecasts but both the headline and trimmed mean estimates are close to the rounding barrier. Full details are below (the paywall).

Measures of non-tradables and domestic market services inflation are expected to have remained quite ‘sticky’ in Q1 at 1.1-1.2% q/q (seasonally adjusted).

The expected increase in aggregate services inflation in Q1 in Australia echoes a similar pick-up in the equivalent measure for the United States.

The expected mix of stronger-than-expected underlying inflation and ‘sticky’ domestic/services inflation will keep the RBA Board firmly on the sidelines. Moreover, signs of labour market resilience (domestically and globally) and an uptick in timely global activity indicators in early 2024 are likely to keep discussion of RBA rate cuts well off the table.

Our view remains that the RBA Board will keep the cash rate at 4.35% until there are clear signs of labour market deterioration. Our best guess is that this won’t happen until at least later this year.