Australia’s Q2 CPI will be released on 31 July, only days before the RBA Board meeting on 5-6 August.

Our bottom-up analysis points to strong prints for both headline and underlying inflation. We covered the relatively strong May monthly CPI here.

We anticipate trimmed mean inflation to have been around +1.0% q/q in Q2, ~0.2ppts above the RBA’s May SMP forecast. Point forecasts and detail are below.

If we are right, this would be the second consecutive quarter that underlying inflation has been above the RBA’s forecasts, and by a decent margin.

In our preview of the May monthly CPI, we concluded that a lot had to go right for the RBA not to hike in August. We viewed markets as significantly under-pricing the risk of an imminent rate hike. Market pricing has now shifted markedly to ~60% chance of an August rate hike.

But there was some good news in the monthly CPI, with more evidence that domestic market services inflation continued to moderate in Q2. Broader non-tradables inflation also moderated a little.

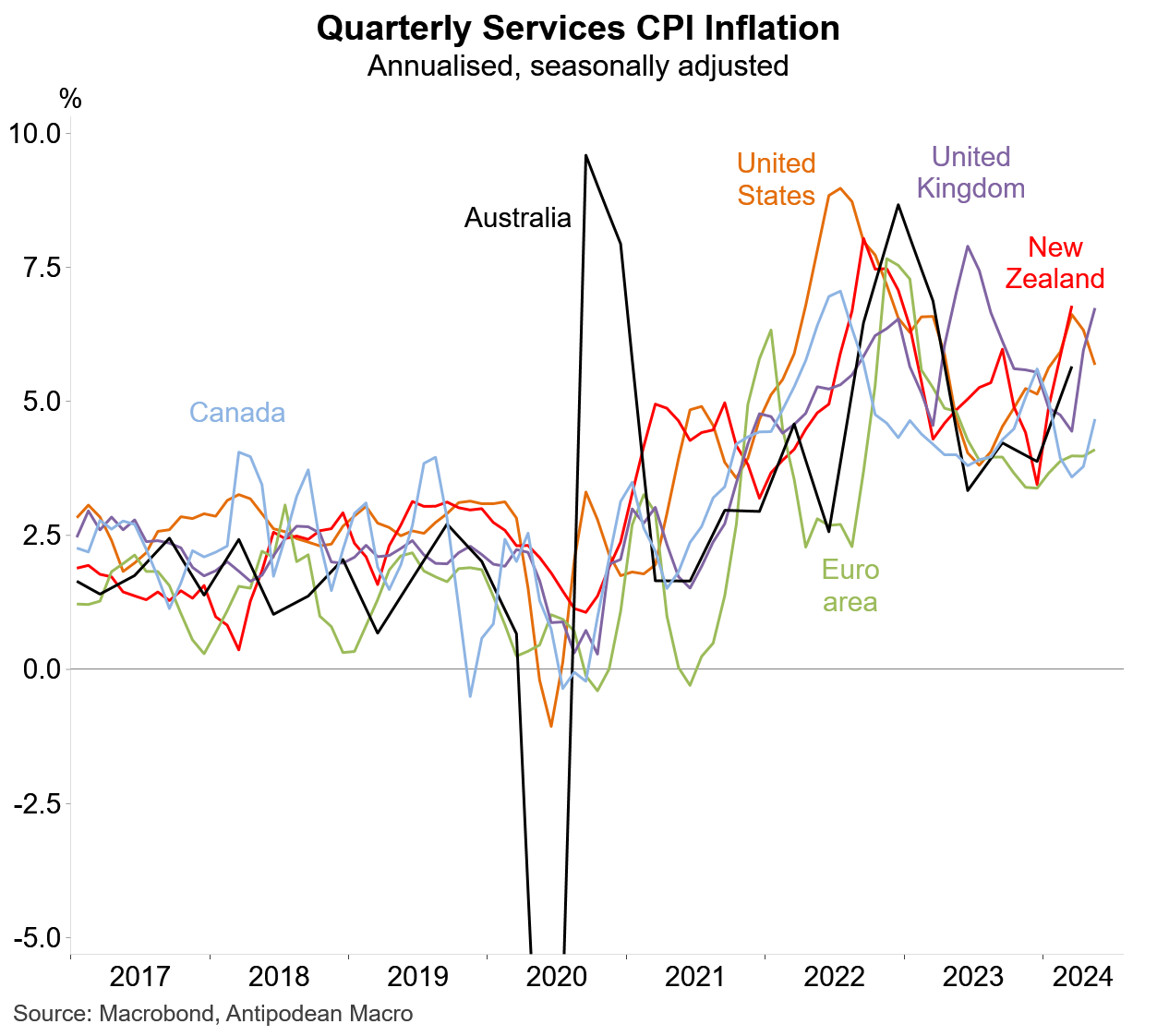

The RBA Board must balance that good news against the likely upside surprise on trimmed mean inflation and the fact that services inflation remains ‘sticky’ in all peer economies (see chart).

We now can’t quibble with market pricing for the August Board meeting. We are in the rate hike camp.

The June labour force report on 18 July is the next important piece of data prior to the full Q2 CPI at the end of the month. The NAB business survey for June released on 9 July also bears close watching.

Whether further monetary policy tightening will be needed after August will (obviously) be driven by incoming data. Critics would point out that one rate hike smacks of ‘fine tuning’, but there is genuinely heightened uncertainty at this point of the cycle. We would expect the Board to again not rule anything in or out after hiking in August.